IndiaP2P Social Impact Performance Report 2025

Our Theory of Change

We believe that our SDG goals can be met only if adequate private sector capital is mobilised i.e. by offering commercial returns.

With a focus on streamlining the lending process and eliminating inefficiencies that exist in the current credit value chain, we aim to make a measurable, positive impact on Sustainable Development Goals (SDGs) 1, 5, 8, 9, and 10. In the future, we hope to have an impact across more SDGs.

We believe that investing in this segment generates outsized profits and impact, however, value chain inefficiencies limit the profits that eventual investors willing to take risk, earn. We solve this by executing the industry’s first end-to-end technology platform.

Sustainable Development Goals enabled

Founders’ Note

FY25 was a year of multiple changes and rapid building. Across the micro/unsecured loan sector, operational challenges emerged alongside new regulations.

We witnessed the once-in many years, deep stress amongst microloan customers compounded by stagnation in incomes. Additionally and simultaneously, we witnessed a major update to NBFC-P2P regulations requiring industry players to undertake major overhauls of their back-end systems and stakeholder communications. These changes demanded a considerable redevelopment of systems while we expanded her physical presence from 29 to 31 districts.

Navigating these changes and challenges has helped us become resilient and deepened our understanding of our users as testing times often do to evolve our suite of products that align better with shifting user needs and ever-changing environments.

With our regulatory update transition completed towards the end of Q3, IndiaP2P was one of the first regulated peer-to-peer lending platforms to introduce the Monthly Income Plan+ in compliance with the RBI's new T+1 settlement rule.

With this update, we have also expanded our field servicing team to service more clients and expand our direct footprint. IndiaP2P was also recognised as a business that is driving positive change with coverage by various media outlets.

With gratitude,

Mohit, Neha, Ravinder and all of us at IndiaP2P

Portfolio at a glance (1/2)

Geographical presence:

We expanded our geographical presence to cover 50 locations across multiple states with physical offices and branches resulting in a 3.8 fold increase in borrowers serviced. Combining digital onboarding & underwriting with proprietary agent-network led channel data, IndiaP2P conducts superior due-diligence while simultaneously serving underserved borrowers.

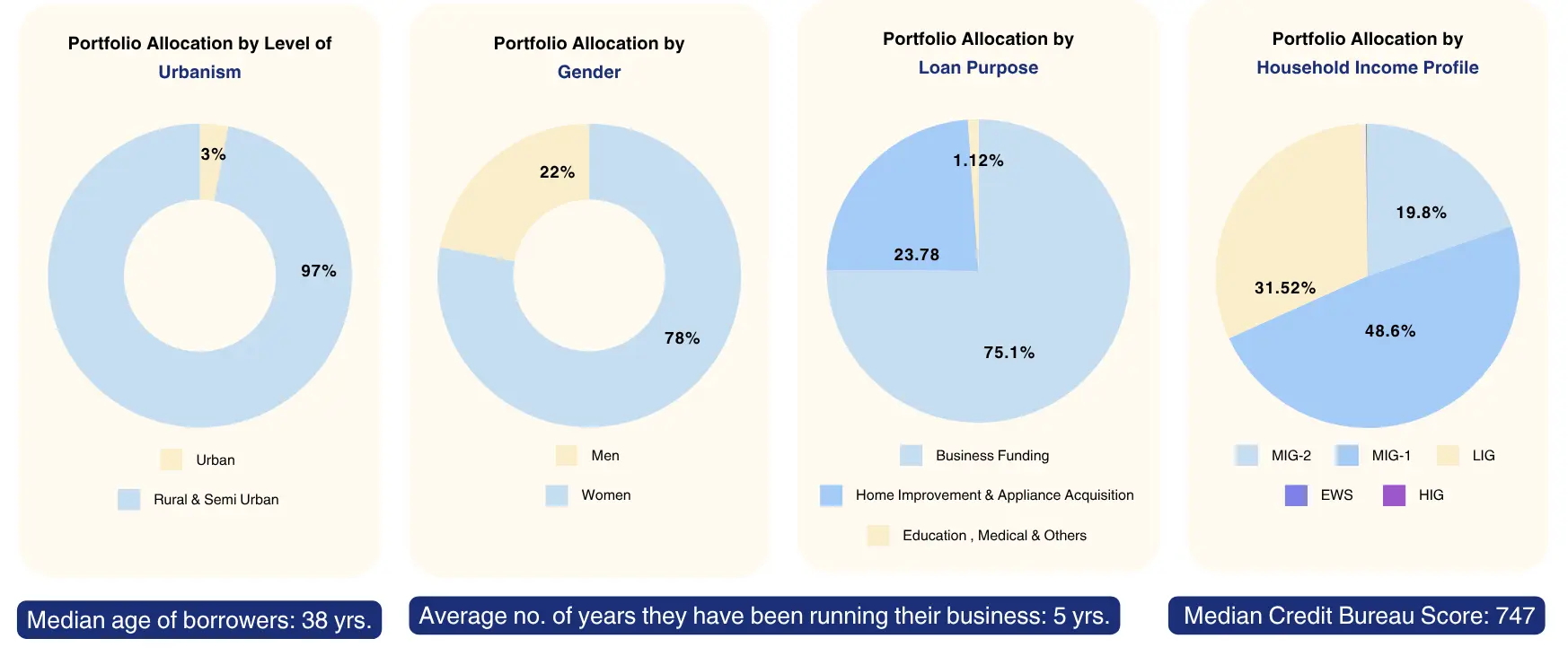

Portfolio at a glance (2/2)

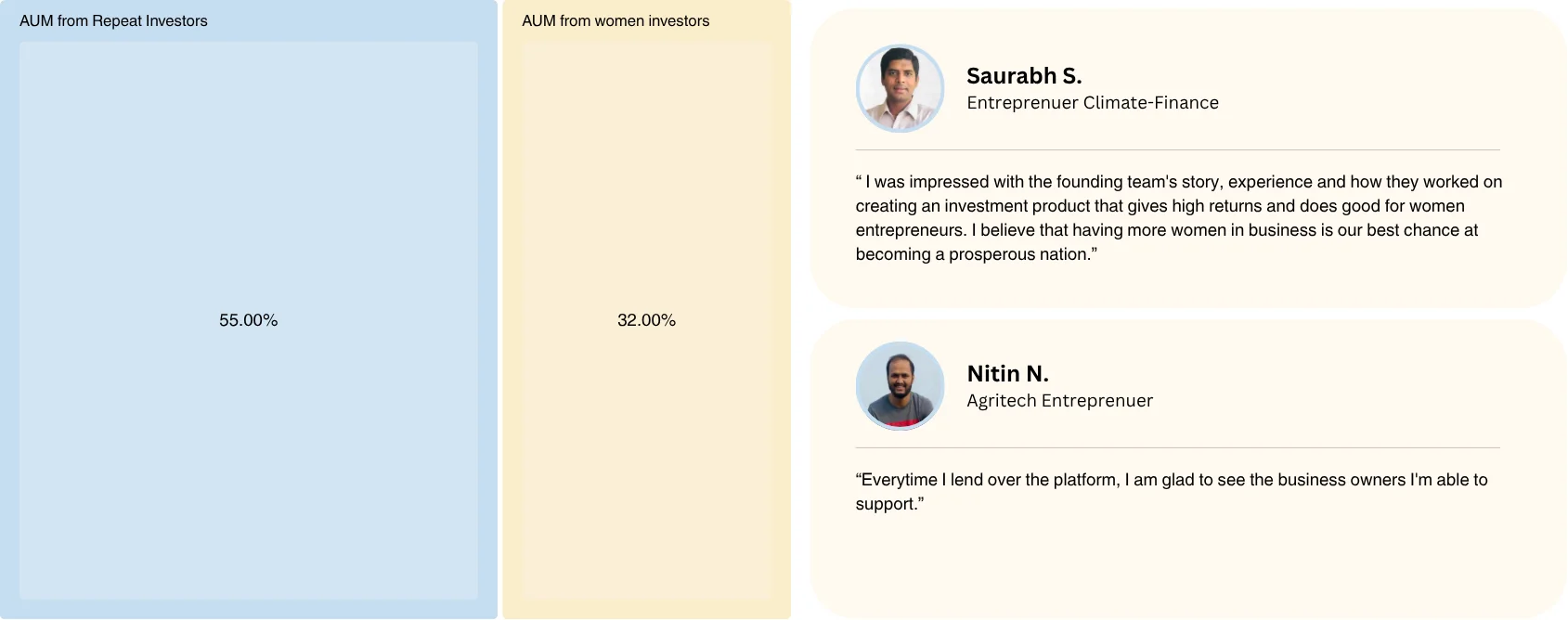

Lender Snapshot

We recognise that retail investors today are increasingly discerning and conscious of the impact of their investment decisions. We are grateful that our mission has attracted lenders from across the country who despite a plethora of investment alternatives available.

SDGs Tracked and Impacted

We track our impact around the UN’s Sustainable Development Goal (SDG) framework with the following SDGs impacted in fiscal year 2024-2025.

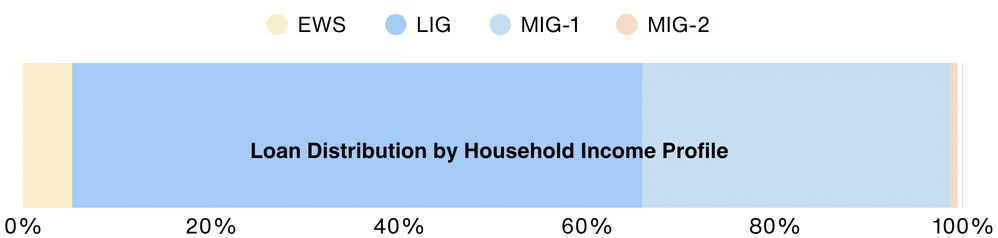

Goal: To end poverty in all its forms everywhere by 2030.

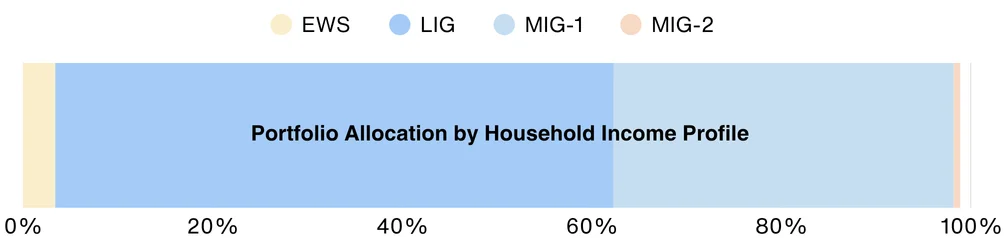

IndiaP2P: 80% loans to lower and middle income households (MIG-1, LIG and EWS)

.webp)

Goal: To achieve gender equality and empower all women and girls.

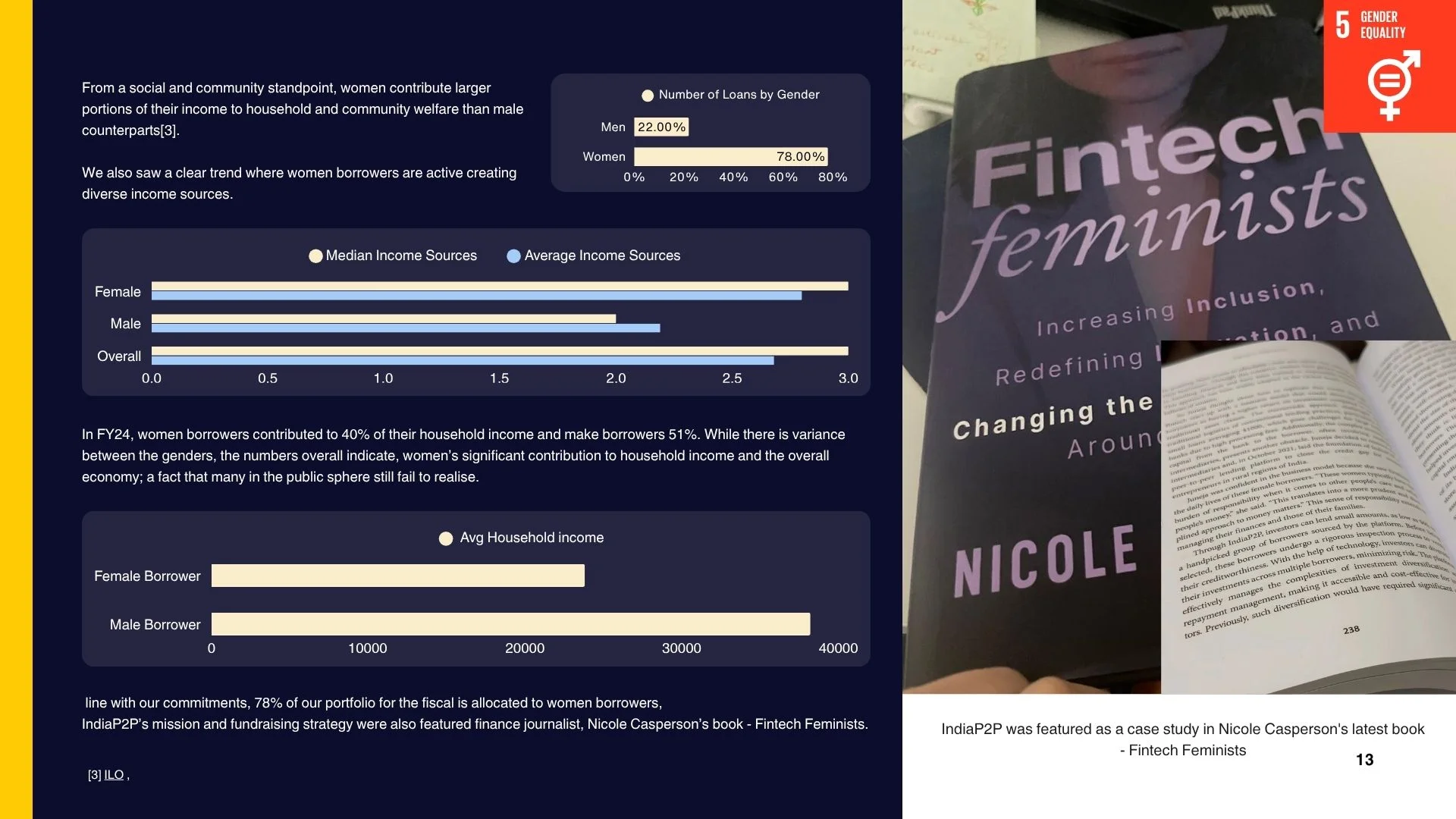

IndiaP2P: 78% loans to women borrowers

.webp)

Goal: To promote inclusive and sustainable economic growth, employment and decent work for all.

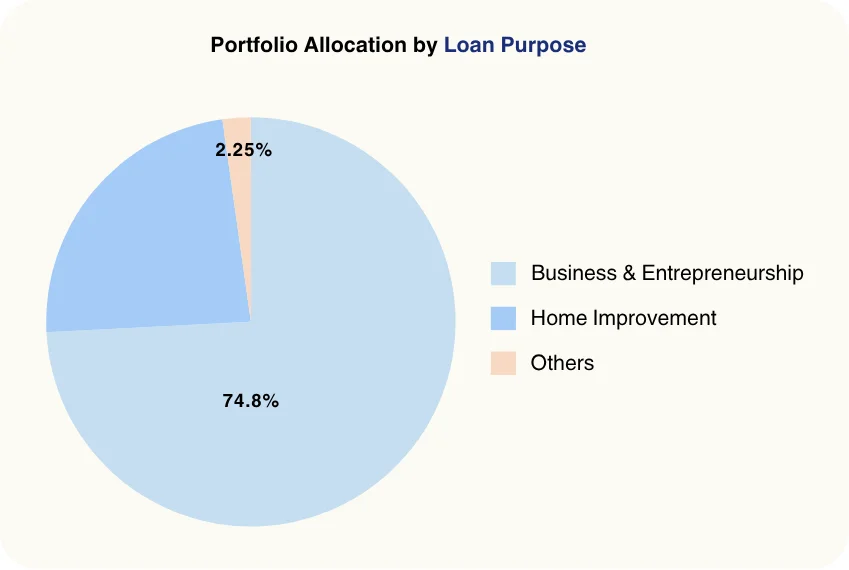

IndiaP2P: 75.1% loans to grow small businesses

Goal: To build resilient infrastructure, promote inclusive and sustainable industrialization and foster innovation

IndiaP2P: Technology infra. to unlock new capital & efficient credit ops.

Goal: To reduce inequalities within and among countries

IndiaP2P: 97% credit flow to underserved rural and semi-urban areas

SDG 1 No Poverty

India’s journey to eradicating poverty is closely tied to improving household incomes—especially for the bottom 90% of its population. According to NITI Aayog and other government data, a significant portion of Indian households continue to subsist on low and irregular incomes. While there has been progress, real income growth for the bottom segments remains sluggish, with inflation-adjusted wages either stagnant or declining in certain sectors. It is estimated that approximately 24.2% of India's population lives on less than $3.65 per day (2017 PPP), according to the World Bank's Poverty and Inequality Platform.

Access to credit plays a critical role in enhancing income resilience. Yet, for a large share of households—especially those running micro and small businesses—credit remains elusive or misaligned. The credit gap becomes even more pronounced when gender is factored in. Women entrepreneurs, particularly in rural and peri-urban areas, are often excluded from formal credit markets due to limited documentation, lack of collateral, or systemic biases.

IndiaP2P directly addresses this structural gap by enabling direct credit access for women-led MSMEs at the smallest ticket sizes. These are precisely the enterprises that contribute significantly to household income and job creation, yet remain underserved.

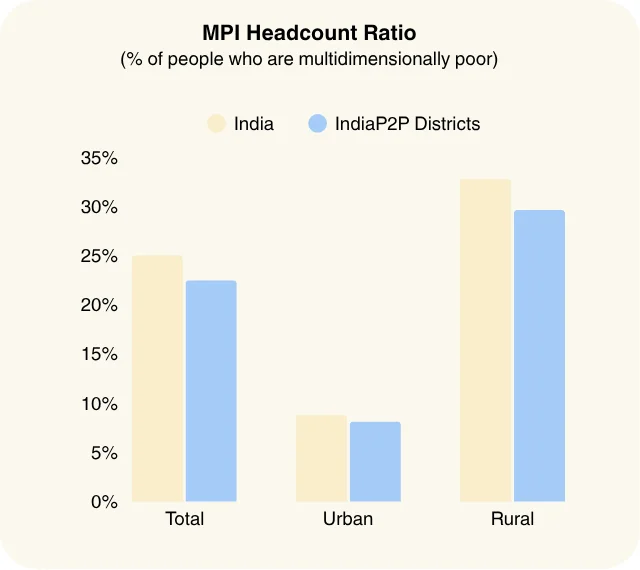

The Multidimensional Poverty Index MPI[2] recognizes poverty as a multidimensional phenomenon, going beyond income or consumption levels to include health, education, and standard of living.

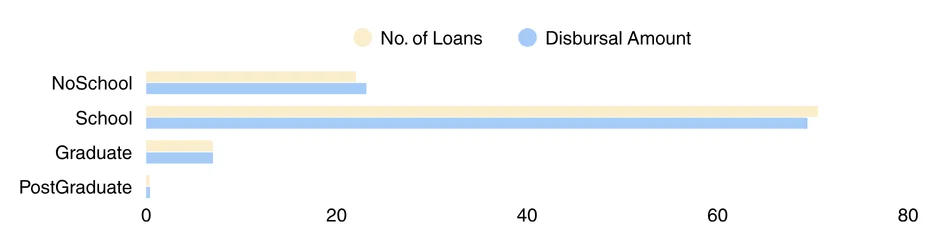

In FY24, IndiaP2P serviced loans to households across 46 locations with a combined MPI ratio of 41.8%. Over half of the households in geographies where IndiaP2P operates are considered poor across at least one category and a quarter are considered multidimensionally poor. IndiaP2P's operations directly contribute to the standard of living of these households.

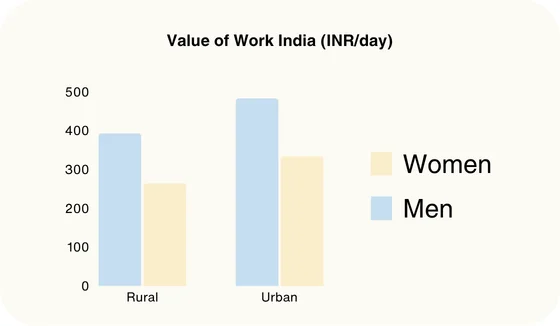

According to MPI data, rural India’s MPI ratio stood at 32.75% whereas urban India’s MPI ratio stood at 8.81% implying that rural India’s poverty ratio is 3.71x of urban India. Realising that, to augment urban-to-rural inflow of capital and credit, IndiaP2P’s portfolio consists of 99% of disbursements in non-urban areas in FY24 and since inception.

SDG 5 Gender Equality

Giving women the credit they deserve. Women-owned businesses in India account for only 20% of all MSMEs, yet their contribution to India’s GDP is disproportionately small—just 3.5%. Despite this, women-led MSMEs have a projected compound annual growth rate (CAGR) of over 20%, signalling significant untapped potential. A key reason this potential remains unrealised is lack of access to credit.

Systemic gender bias—both implicit and structural—continues to limit financial access for women. As Mary Ellen Iskenderian outlines in There's Nothing Micro About a Billion Women, female entrepreneurs are more likely to be denied loans or offered smaller ticket sizes, even when their financial credentials match those of their male counterparts.

IndiaP2P exists to change this. With women-led micro-enterprises at the heart of our model, we deliver precisely what traditional finance has failed to do: fair, fast, and flexible credit to India’s most overlooked asset class.

SDG 8 Decent Work and Economic Growth

India’s MSMEs form the backbone of its economy, contributing nearly 30% of GDP and employing over 110 million people. Yet, a vast segment of these businesses—especially those run by women—operate below their potential due to lack of timely, affordable credit. The credit gap for India’s MSME sector is estimated at ₹25 trillion (~$300 billion).

IndiaP2P exists to change that. By focusing on loan sizes under ₹2 lakh and on enterprises led by women, we serve the exact segment that India’s formal financial system has left behind. Our tech-led infrastructure and risk-pricing tools allow us to deliver credit efficiently and responsibly to this “invisible middle.”

SDG 9 Industry, Innovation, and Infrastructure

IndiaP2P is bridging this gap with a technology-led infrastructure designed for accessibility, speed, and trust. Our platform enables individual lenders to participate in funding high-potential micro and small enterprises, while our borrower-side processes are optimised for ease of use and minimal friction.

We’ve co-developed solutions with on-ground teams to ensure that onboarding, repayment tracking, and communication are seamless and adapted to regional needs. Our system doesn’t rely on traditional proxies like credit scores alone, but incorporates behavioural and business data to better assess creditworthiness.

SDG 10 Reduced Inequalities

One of the most persistent drivers of inequality in India is uneven access to formal finance. The top tiers of the credit market continue to grow rapidly, while a large section of credit-worthy but non-standard borrowers remains excluded.

IndiaP2P helps correct this imbalance by unlocking capital for the most credit-excluded segments through digital distribution and data-led underwriting. Our model enables thousands of small business owners—many from rural districts—to access capital without being penalised for geography, gender, or informality.

Over 99% of our portfolio was allocated to non-urban areas in FY25. 78% went towards women. IndiaP2P’s targeted lending acts directly on SDG 10.2 and 10.4.

Recent Reports

See all

IndiaP2P Social Impact Performance Report 2024

Unlock capital and bridge the credit gap for rural and semi-urban women-led businesses with IndiaP2P. Transform financial futures and support SDGs with impactful investments. Read more

IndiaP2P Social Impact Performance Report 2023

Indiap2p Social Impact Performance Report Read more